PFE Stock: Performance Data & The Real Outlook

Pfizer's Numbers Game: Is the Bottom In, or Just a Deep Discount?

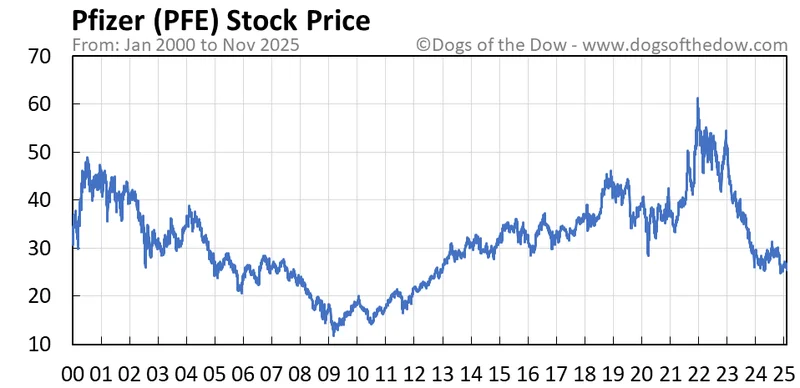

The market’s a funny place, isn’t it? One day, everyone’s chasing the next big thing, pouring money into anything with "AI" or "disruptive tech" in its description. The next, they’re sifting through the wreckage, looking for a bargain. And right now, a lot of eyes, including mine, are on Pfizer (PFE). On November 10, 2025, the stock nudged up a measly $0.010, closing at $24.43 – a 0.041% gain. Barely a ripple in the grand scheme of things, especially when you consider its -1.4% return over the past month, lagging behind the Zacks S&P 500 composite’s modest 0.3% gain. It’s a performance that mirrors its Large Cap Pharmaceuticals industry peers, which also stumbled 1.4%. So, why the sudden chatter? Why is Pfizer attracting investor attention, becoming one of the most-watched stocks on Zacks.com, as highlighted by Pfizer Inc. (PFE) is Attracting Investor Attention: Here is What You Should Know - Yahoo Finance? The answer, as it often is, lies in the numbers, but not just the ones on the surface.

The Allure of the Anchor and the Shifting Sands of Estimates

You don’t have to squint too hard to see the primary draw: that dividend. At an approximate 7.04% yield, dishing out $0.43 per share quarterly, it’s a robust payout. For income-focused investors, it’s like finding a sturdy anchor in a choppy sea, offering compelling compensation and, theoretically, a degree of downside protection. This isn’t new territory for Pfizer; the company boasts a consistent track record of dividend payments through various market cycles. It makes sense, then, that institutional investors are starting to notice what they perceive as "valuation disparities," eyeing PFE as an attractive entry point for defensive exposure with potential upside. They’re seeing a classic mean-reversion candidate, a giant that’s been beaten down to historically attractive valuations (its market capitalization sits around $138.90 billion, which, for a company of its stature, trades at attractive multiples compared to historical averages, and at discounted valuations across multiple metrics compared to its industry peers).

But here’s where my skepticism kicks in, or rather, where the data starts to get a little… squishy. Let’s talk earnings estimates. For the current quarter, the consensus is $0.66 per share, a projected +4.8% change from the year-ago quarter. Sounds good, right? Except the Zacks Consensus Estimate changed -8.6% over the last 30 days. Think about that for a second. Analysts were significantly more optimistic just a month ago. For the current fiscal year, the estimate is $3.13, a +0.6% change from prior year, with a +2.4% change over the last 30 days. Then, next fiscal year, it's $3.14, a +0.3% change from a year ago, but with a -0.4% change over the past month.

I’ve looked at hundreds of these estimate shifts, and the choppy movement here is genuinely intriguing. What exactly are these analysts seeing, or not seeing, that causes such month-to-month volatility in projections, even as the year-over-year growth figures remain stubbornly flat? It suggests a lack of clear visibility, doesn't it? A Zacks Rank #3 (Hold) (meaning analysts largely expect it to perform in line with the market, not spectacularly, not terribly) perfectly encapsulates this ambiguity. This isn't just a minor statistical blip; it reflects broader investor skepticism regarding traditional pharmaceutical companies' ability to generate sustainable growth following the COVID-19 pandemic windfall. The market remembers the gold rush, and it's asking: "What's next, really?"

The Catalysts and the Calculus of Comeback

Pfizer's management isn't sitting still. They’ve implemented recent cost-cutting initiatives and portfolio optimization strategies. The company also recently beat Q3 earnings estimates by an impressive 32%, which is a significant positive signal, suggesting operational efficiency might be better than expected, or perhaps estimates were just too low (a common trick, I’ve found, to create a positive surprise). Upcoming pipeline updates and guidance revisions are expected to serve as significant catalysts for stock performance. Technical indicators are even whispering about a potential trend reversal, with the stock establishing higher lows and volume patterns hinting at institutional accumulation. Pfizer (PFE) stock poised for potential turnaround - Rolling Out It's almost as if the smart money is quietly building positions, betting on that mean-reversion.

But is that enough? My analysis suggests that while the dividend offers a compelling floor, the real upside hinges on those "pending catalysts" delivering actual, quantifiable growth beyond the meager single-digit percentage points currently projected. We’re not just talking about incremental improvements; we need a significant narrative shift. The market isn’t giving Pfizer the benefit of the doubt on growth, and for good reason. The post-pandemic hangover is real, and the question isn't just if they have a pipeline, but how big that pipeline is, and when it translates into revenue that moves the needle on a $138.90 billion (to be more exact, $138.90 billion, not just "around $139 billion") market cap. The stock might be discounted, yes, but often, discounts exist for a reason. Is the market simply too slow to price in these future wins, or is there a fundamental, unaddressed growth problem lurking beneath the surface that only a few are truly seeing?

The Waiting Game's True Cost

The investment thesis for Pfizer right now feels like a high-stakes waiting game. You're paid handsomely to wait, no doubt, but what are you waiting for exactly? A genuine, sustainable growth engine to ignite, or just for the market to eventually "catch up" to its historical valuation? Technical indicators and institutional interest are one thing, but the fundamental earnings projections, with their internal contradictions and recent downward revisions for future periods, tell a different story. They suggest a company still searching for its post-COVID identity, trying to balance cost control with innovation. It's a tightrope walk, and while the dividend offers a safety net, it doesn't guarantee the performance.

The Yield Trap's Shadow

Related Articles

China's SSE Index Upgrade: Why This Signals a New Era for Global Tech & Finance

I spend most of my days thinking about the future. I look at breakthroughs in quantum computing, AI,...

NIO Stock: What's Next After Earnings

The hushed buzz of the trading floor, usually punctuated by sharp cries, held a momentary breath as...

John Malkovich Cast as President Snow: An Analysis of the Casting and Its Implications

The announcement landed with the precision of a well-funded marketing campaign. The Hunger Games, a...

palantir: what we know

The Math Doesn't Add Up: Why Everyone's Wrong About This Let's cut the crap, shall we? I'm seeing a...

Tax Reimagined: Income, Property, and Capital Gains – What the Future Holds for Your Finances

The Future's Blueprint: How We Tax Today Shapes the Innovations of Tomorrow Here’s a truth we often...

Primerica: A Sober Look at the Numbers Behind the Business Model

Generated Title: Aetherium AI's 5 Million Users: A Masterclass in Misdirection The venture capital w...